Why a Monthly Finance Ritual Beats “Once-a-Year Panic”

Many owners only look hard at their numbers once a year—usually when tax season forces them to. By that time, it’s too late to course-correct.

Multiple sources argue that monthly financial reviews are one of the most effective habits you can build:

-

The U.S. Chamber of Commerce recommends monthly monitoring of key financial reports to measure health and outlook.

-

Accounting firms note that monthly financial statements allow you to spot trends and issues early, rather than looking backwards at the end of the quarter.

-

Advisory articles on financial reviews stress that regular check-ins help identify risks and growth opportunities before they become emergencies.

The good news: you don’t need to become a spreadsheet wizard. You just need five key numbers and 60–90 minutes each month.

Let’s walk through them.

Number 1: Ending Cash Balance (and Cash Runway)

If you only looked at one number, this would be it.

What it is:

Your ending cash balance is how much money is in all your business bank accounts at the end of the month, after deposits and payments clear.

Why it matters:

-

Cash is oxygen. You can be profitable on paper and still fail if you run out of cash.

-

Research repeatedly shows cash flow problems are the leading cause of failure—one study cited by SCORE and others attributes 82% of small business failures to cash flow issues.

How to use it:

-

Record ending cash each month (including savings, not just checking).

-

Divide by your average monthly operating expenses (e.g., rent, payroll, software, utilities, etc.).

-

The result is your cash runway in months.

Example: You have $90,000 in cash and spend about $30,000 per month. Your runway is 3 months.

Rules of thumb:

-

Aim for 2–3 months minimum runway as a baseline.

-

If you’re in a volatile industry or growing fast, 3–6 months is safer.

If your runway is shrinking month over month, you have an early warning sign—and time to adjust.

Number 2: Monthly Recurring Revenue (or Core Revenue)

Revenue can be noisy. To make it useful, define your core recurring revenue, even if you don’t run a subscription business.

What it is:

- For subscription/retainer businesses: your Monthly Recurring Revenue (MRR).

- For project/contract businesses: the typical monthly revenue from your core offerings, excluding one-off, abnormal spikes.

Why it matters:

- It tells you what you can reasonably count on next month.

- It helps you understand if growth is real or just the result of a big one-off contract.

How to use it:

- Track total revenue and core recurring revenue separately.

- Watch trend lines: is recurring revenue growing, flat, or declining?

Even a simple line chart over 12 months can tell you whether your business is becoming more stable or more fragile.

Number 3: Gross Margin

Too many owners obsess over top-line revenue but ignore gross margin—the percentage you keep after direct costs (like subcontractors, materials, or direct labor).

What it is:

Gross Margin = (Revenue – Cost of Goods Sold) ÷ Revenue

This number tells you how much is left to pay overhead and profit after delivering your service or product.

Why it matters:

- You can double revenue and still be worse off if your margin drops.

- It’s a key metric for pricing decisions and cost control.

How to use it:

- Calculate your gross margin each month.

- Compare it to previous months and to your target.

- When margins dip, look for causes: discounting, scope creep, overtime, rising supplier costs.

If you’re a service business, your “cost of goods sold” often includes billable staff wages, subcontractors, and any direct project costs.

Number 4: Operating Profit (or EBITDA) – and the Trend

Operating profit (or EBITDA for a more standardized view) tells you whether your core operations are actually making money once you’ve paid for overhead.

What it is:

- Operating profit = Gross profit – operating expenses (rent, admin salaries, marketing, software, etc.).

- EBITDA adds back interest, taxes, depreciation, and amortization for a cleaner comparison across time.

Why it matters:

- Many owners look at bank balance and revenue but ignore whether they’re truly profitable.

- Tracking profit month-to-month shows whether your growth is actually sustainable.

How to use it:

- Track operating profit in dollars and operating margin (profit ÷ revenue).

- Plot 3–6 months of operating profit in a simple chart.

You want to see:

- Fewer loss-making months over time

- A gradually improving margin as you refine pricing and process

If revenue is rising but profit is flat or shrinking, that’s your cue to review pricing, scope, or overhead.

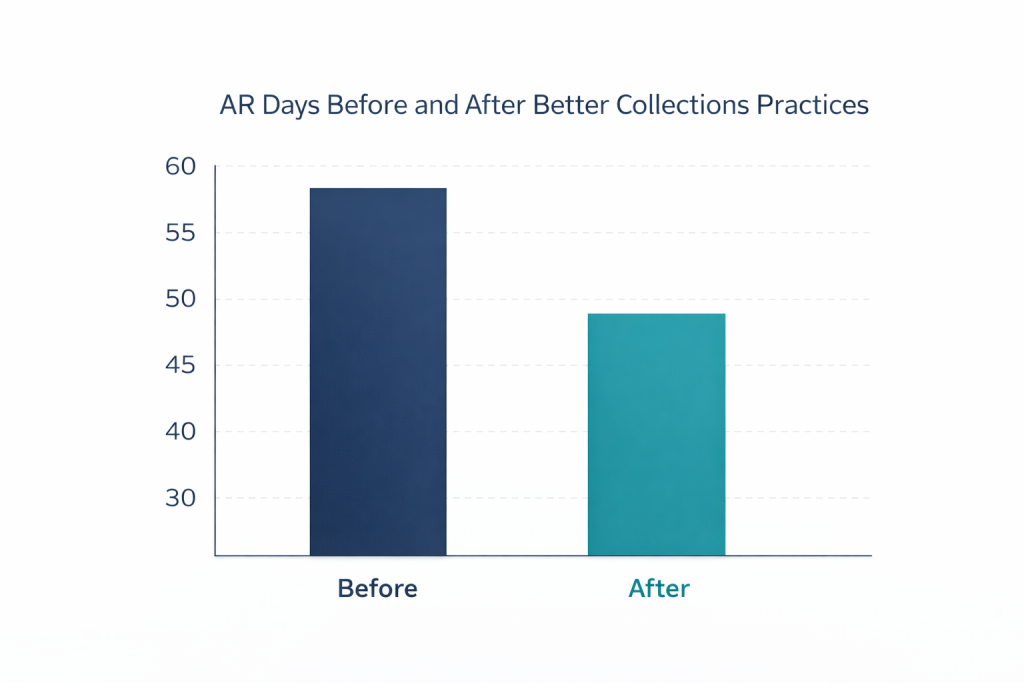

Number 5: Accounts Receivable Days (How Long It Takes to Get Paid)

You can have great sales and margins and still struggle if customers pay slowly.

What it is:

- Days Sales Outstanding (DSO) or AR Days measures how long it takes, on average, for you to collect payment.

DSO ≈ (Accounts Receivable ÷ Monthly Credit Sales) × 30

(You don’t have to be exact—an estimate is enough for small businesses.)

Why it matters:

- Slow collections choke cash flow.

- Tightening AR can be one of the fastest ways to improve cash without cutting anything.

How to use it:

- Calculate your AR days monthly.

- If it’s significantly higher than your payment terms (e.g., 45+ days on “Net 30” terms), you have a collections issue.

- Experiment with:

- Deposits or progress billing

- Faster invoicing

- Automatic reminders

- Card/ACH payment links on invoices

Even shaving 5–10 days off your AR can meaningfully boost cash.

Putting It All Together: A 60-Minute Monthly Review Ritual

Here’s a simple monthly ritual you can implement today:

- Block 60–90 minutes on your calendar for a “Finance Review” (ideally the same day each month).

- Print or open (a) your P&L, (b) balance sheet, and (c) cash flow statement for the month.

- Fill out a one-page worksheet with:

- Ending cash & runway

- Core recurring revenue

- Gross margin %

- Operating profit & margin

- AR days

- Add three quick notes:

- What looks better than last month?

- What looks worse?

- What 1–2 actions will I take this month as a result?

Keep this simple. Consistency beats complexity.

The Take-Home Message

You don’t need 50 KPIs. You need a small, sharp dashboard that you actually look at.

By reviewing just these five numbers each month:

- Ending cash & runway

- Core revenue / MRR

- Gross margin

- Operating profit

- AR days

…you’ll see trouble months earlier, not after it’s too late to respond.